Overview

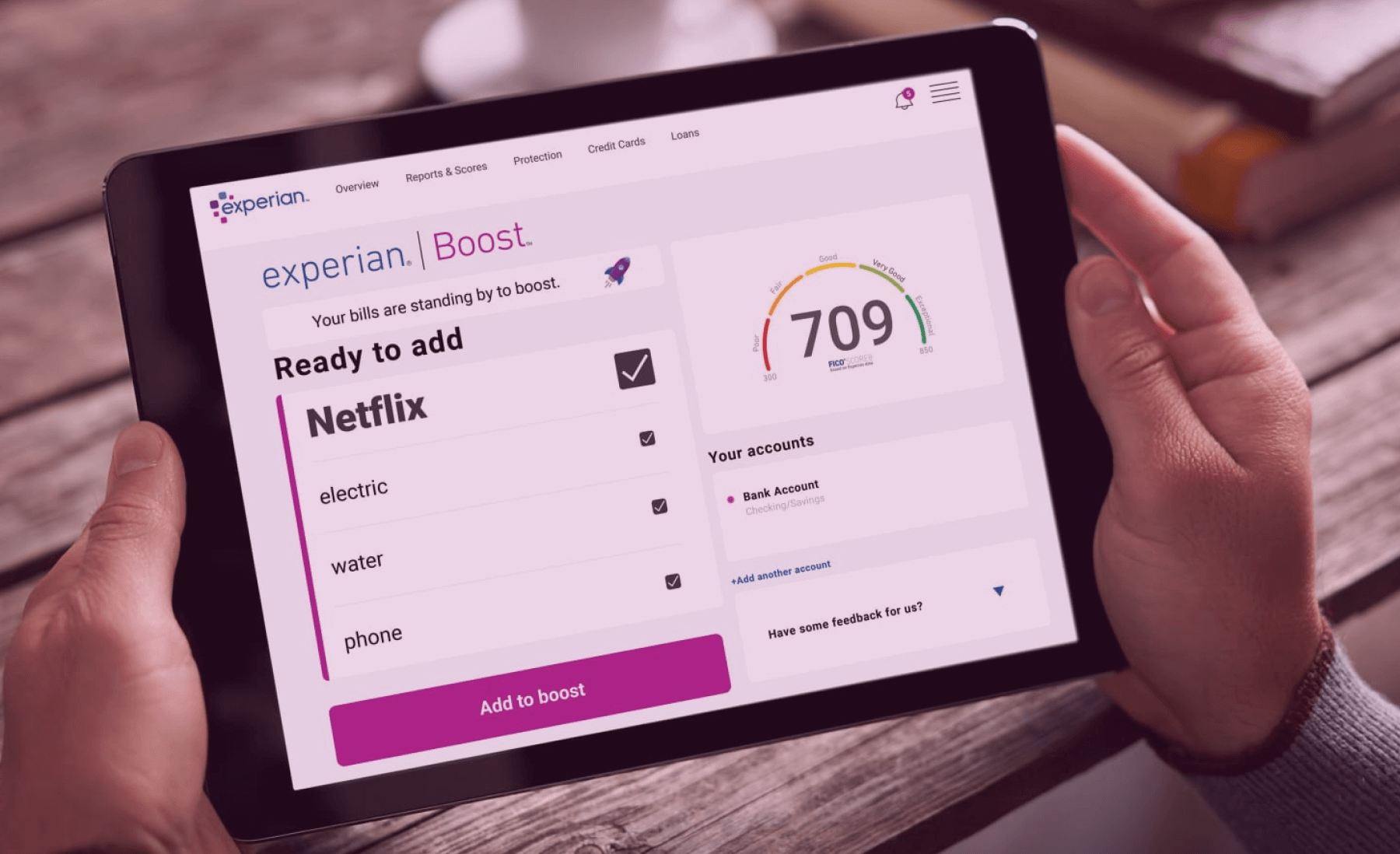

What if paying for your Netflix subscription could help you buy a home? We turned this question into reality with Experian Boost, improving the opportunities for everyday bill payments to build credit scores. By recognizing the bills people have already paid from utilities to streaming services, we have helped millions of credit-invisible Americans be recognized for their financial responsibility and unlock financial opportunities that were previously out of reach. By integrating with the UltraFICO™ Score system and forming partnerships with over 30 financial institutions, our work resulted in an average 13-point score improvement for more than 35 million Americans.

RESEARCH & DESIGN

Design research · Mobile-first product design · Fintech regulatory compliance · Secure banking integration

- Duration: October–March 2019

- Partners: FICO®, Finicity, MasterCard

- Team: Fas Lebbie, John Adam, Brian Burgess, Experian Design Team

Confidentiality: This case study reflects my design perspective and approach. Details have been modified to protect sensitive information while showcasing methodology.

WHAT I BROUGHT

As a design lead reporting to the VP of Design, I spearheaded design research. I developed and deployed qualitative and quantitative research methods to conduct product and user research on alternative credit paradigms through UltraFICO™ integration.

I designed web and mobile interfaces for Boost features in a highly regulated industry, utilizing data from the mortgage and rent industries. This integration enabled the UltraFICO™ Score system across 30+ financial institutions, achieving 92% user trust ratings and regulatory compliance.

Led cross-functional partnerships with FICO and Experian in driving industry-wide transformation through strategic partnerships and new paradigms, shifting traditional credit evaluation to alternative data recognition and benefiting 35 million Americans nationwide.

Problem Context

The current U.S. credit scoring system faces challenges, with 53 million consumers having little to no data and 79 million having FICO® credit scores below 680. This issue highlights gaps in assessing creditworthiness, particularly in light of modern financial behavior. Many consumers who regularly pay utilities, streaming services, and phone bills find traditional models disregard these responsible actions. This discrepancy arises from a credit evaluation framework that is not aligned with contemporary practices, resulting in inequitable credit access. Experian recognizes the need for an approach that includes alternative data sources. By incorporating non-traditional financial behaviors, we developed the opportunity for a more inclusive system that better reflects creditworthiness.

My Approach

With a focus on designing an impact instead of a product, I approached this project by starting with real people’s stories. I gathered user data through interviews, taking on the role of an investigative journalist. This strategy shaped our design process, allowing us to gain a holistic perspective and create more relevant interventions with real-world impacts.

Our first step towards a focused HMW question and research objective was to understand the concept of “thin” files in the financial sector, where approximately 53 million Americans lack sufficient credit histories for traditional scoring models. Many individuals display financial responsibility through regular bill payments but are overlooked by conventional credit systems. By utilizing primary data, secondary data, and insights from research participants, we explored how to leverage alternative payment data to transform these overlooked behaviors into valid indicators of creditworthiness. By understanding thin files and the surrounding system, we grounded the research in the realities of the individuals most affected: young adults, immigrants, and lower-income individuals who had previously been deemed invisible by standard methods.

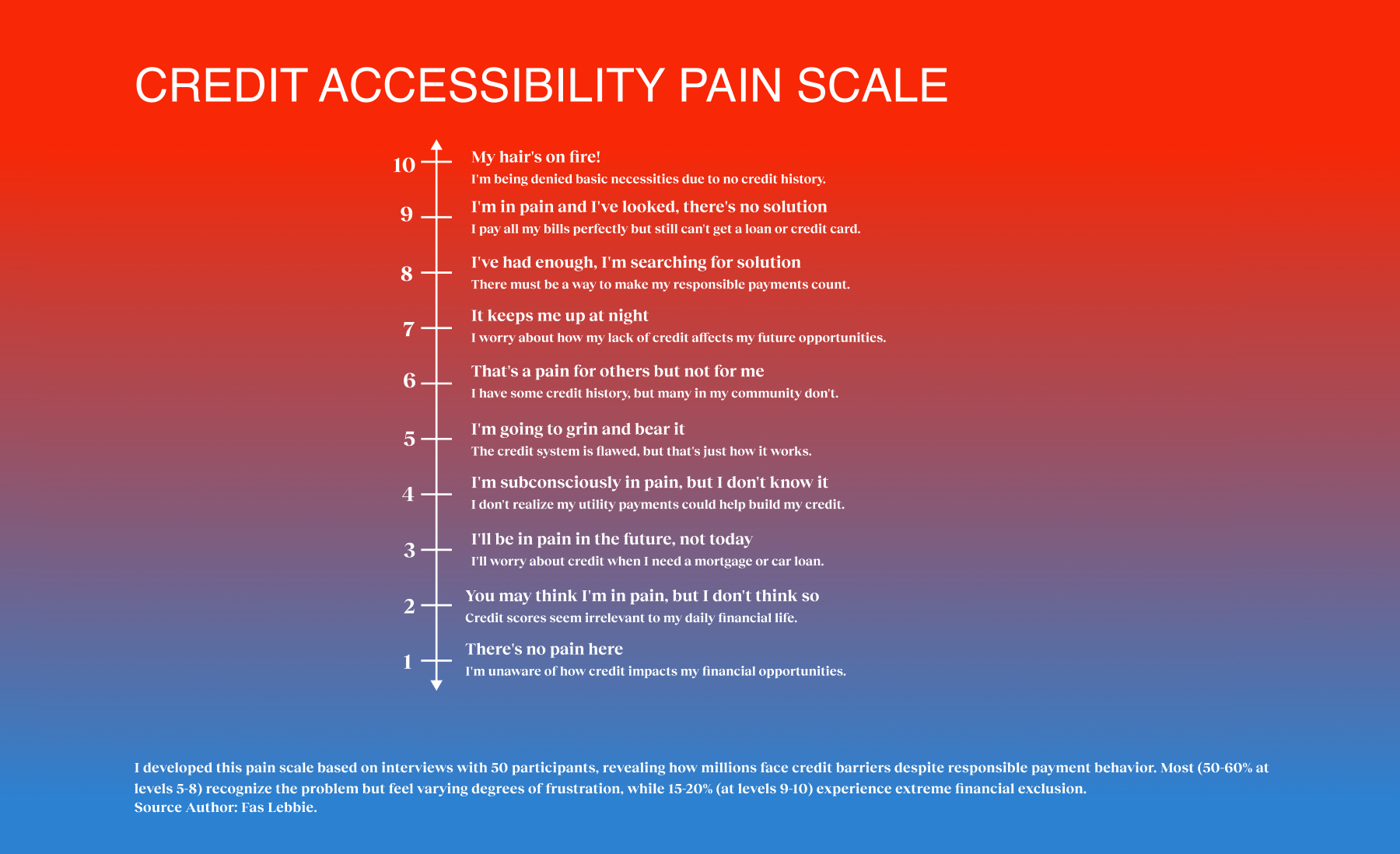

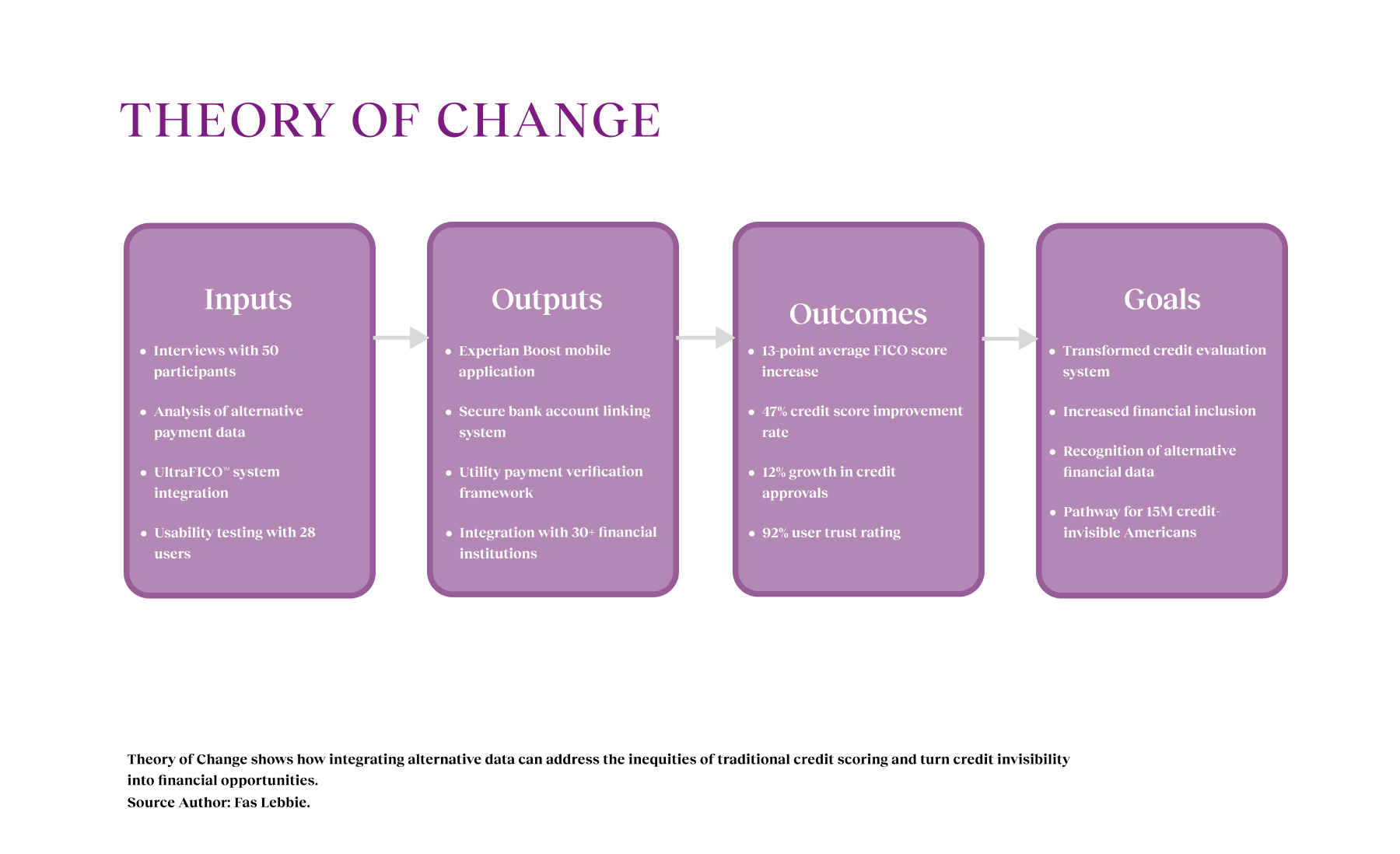

The research employed an ethnographic approach, conducting one-on-one structured and semi-structured interviews with 50 participants to explore the financial inclusion challenges faced by marginalized communities, young individuals, and middle-aged adults struggling with credit. Each 30-to 60-minute interview revealed personal stories that highlighted key insights. The complementary quantitative analysis revealed over $50 billion in unacknowledged monthly utility payments, validating our findings. To refine the solutions further, we engaged 28 users in iterative usability testing, ensuring that our design was simple, transparent, and immediately beneficial, while addressing emotional barriers and trust concerns related to financial data sharing.

This research identified opportunities to bridge the gap between reliable bill payment data and creditworthiness indicators. Participants managed utility payments and financial commitments but received no acknowledgment of their financial behavior. Our research found that 90% of participants had a low rate of large purchases that build credit but a high rate of consistent utility and rent payments. These participants reflected the 35% of Americans, whose monthly rent and utility payments do not contribute to their credit scores. These payments total over $50 billion annually. Most participants maintained a thin file, yet their bill payments reflected actual creditworthiness.

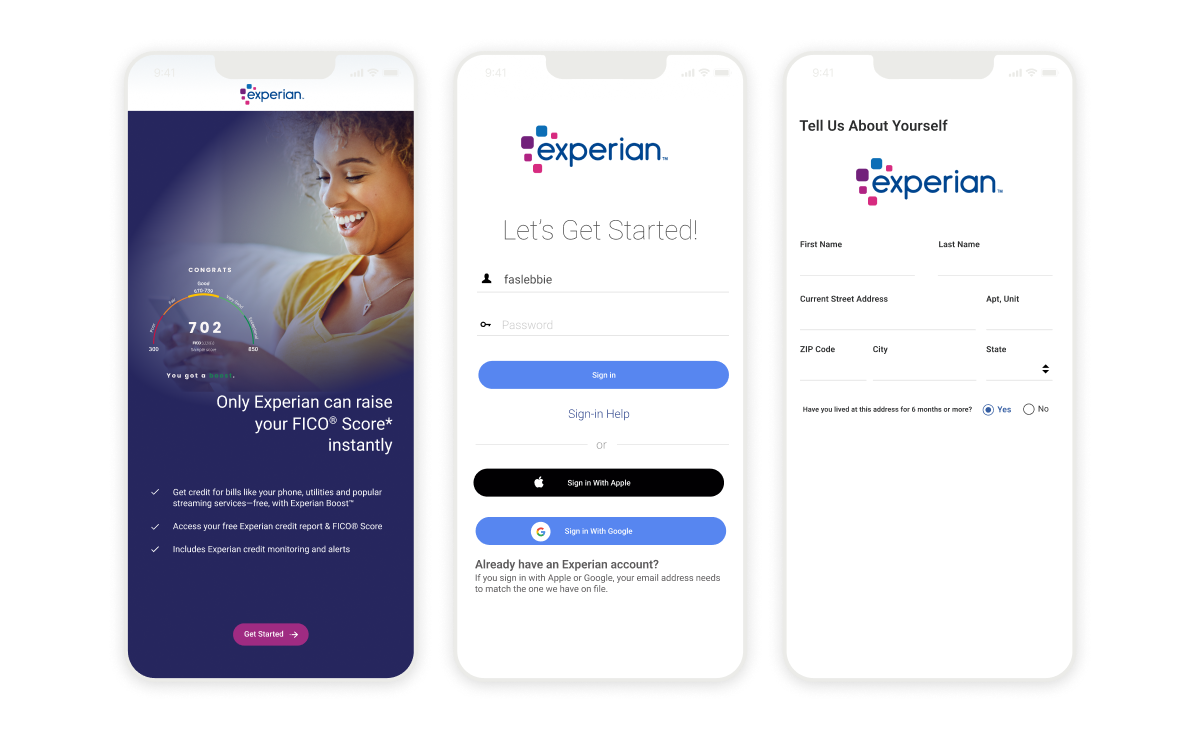

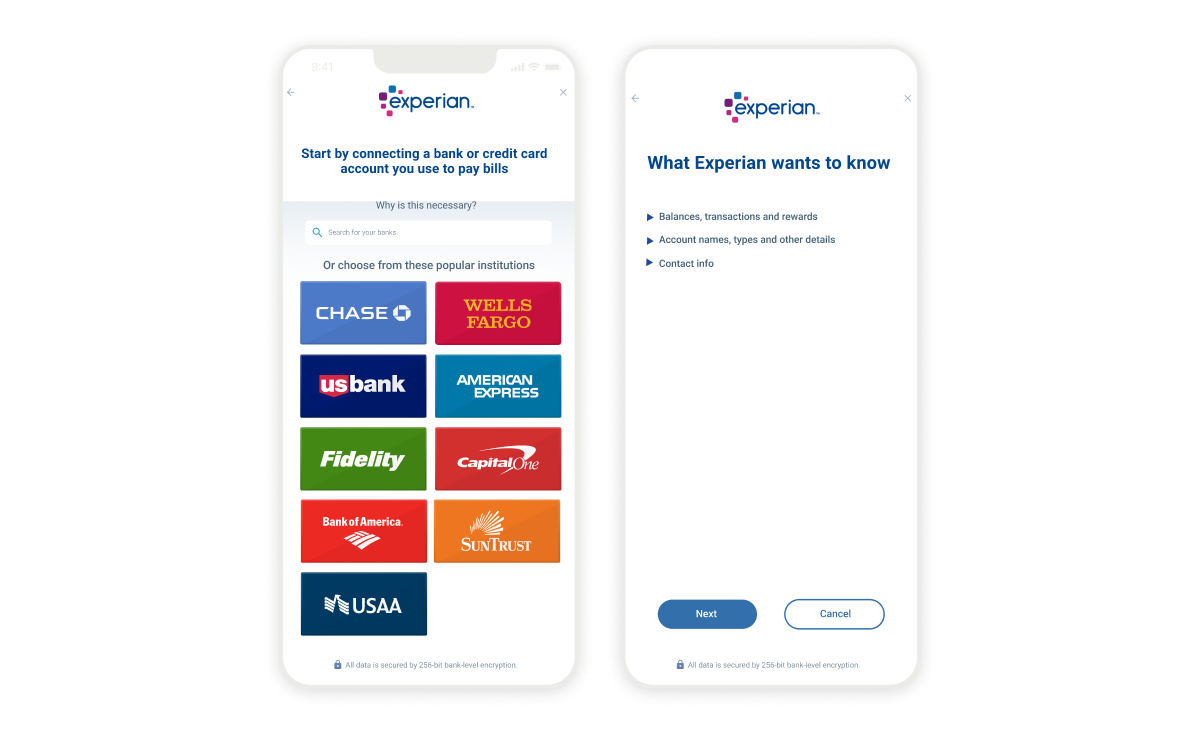

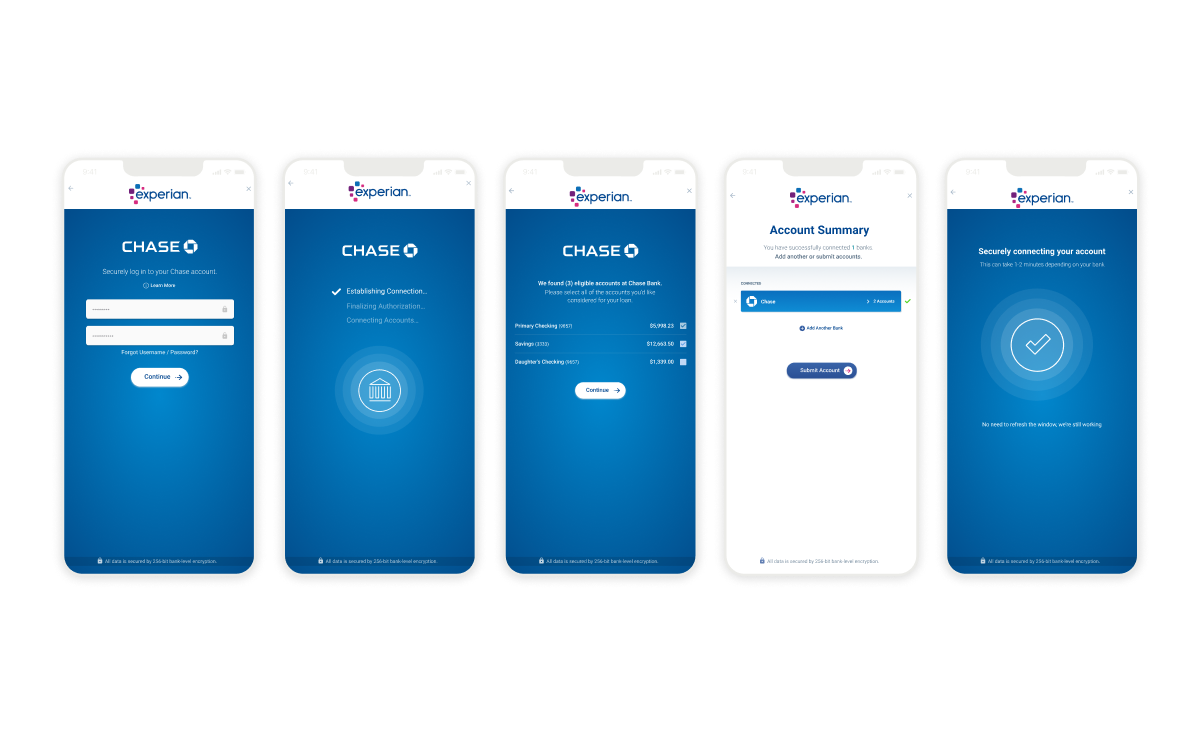

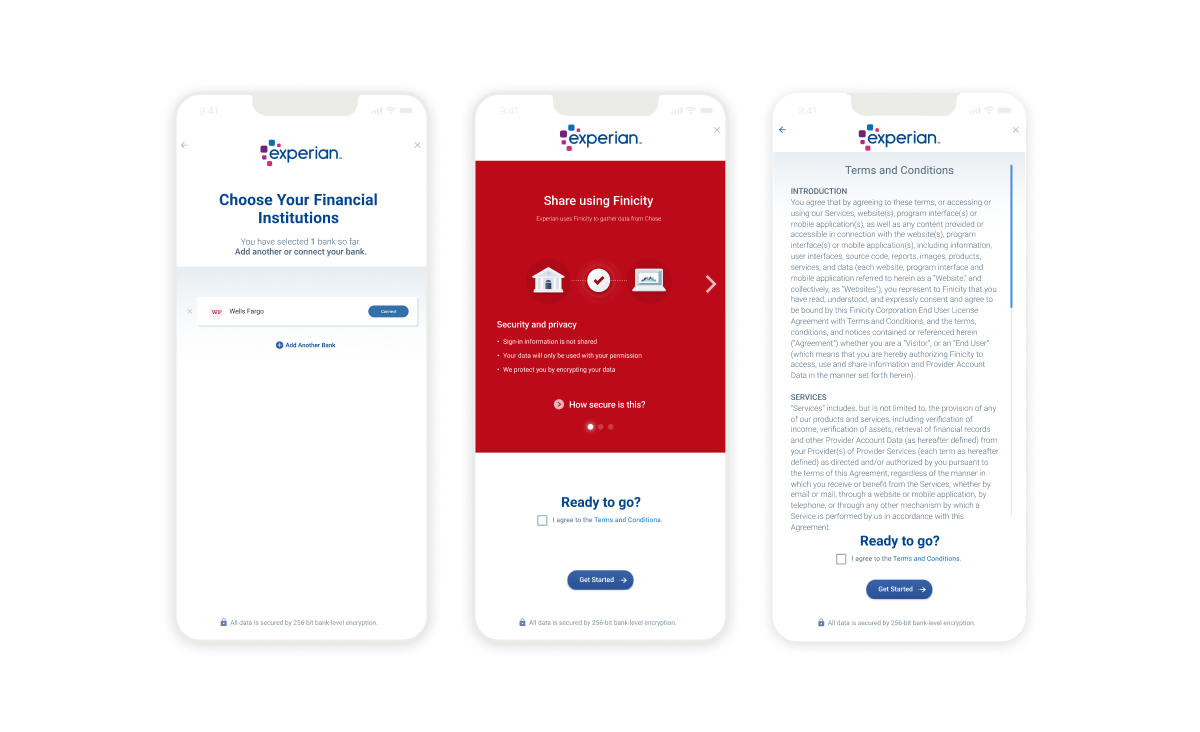

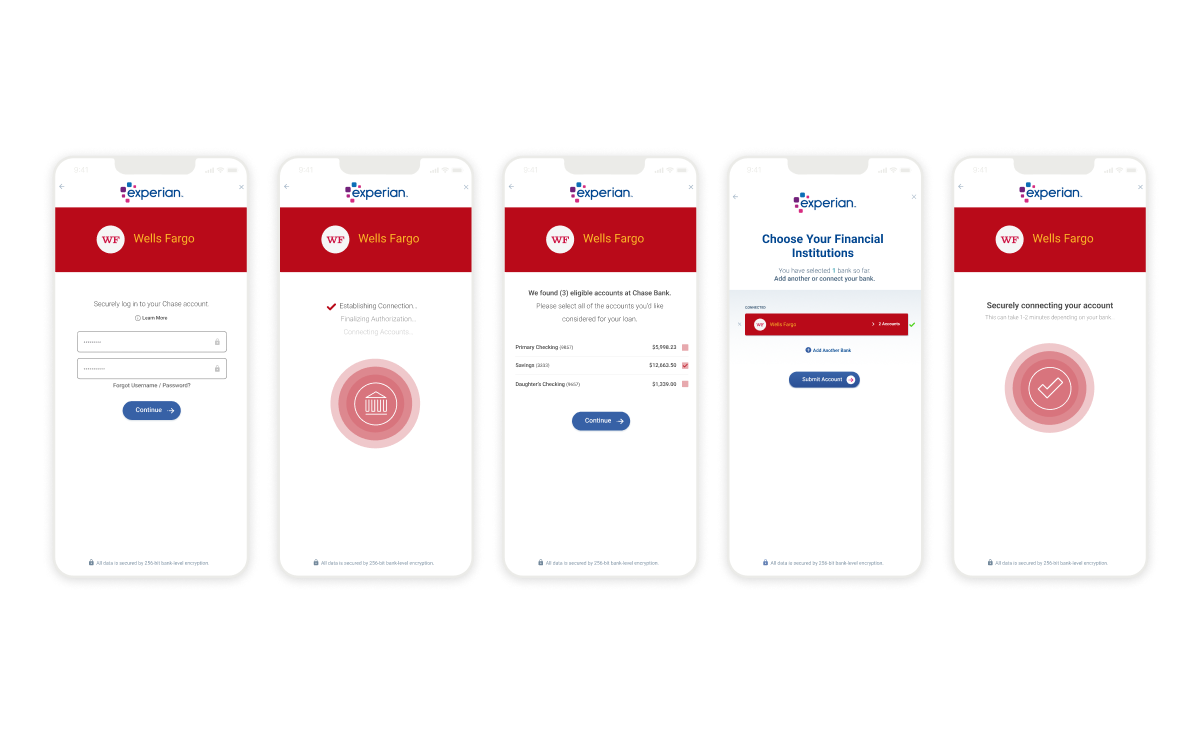

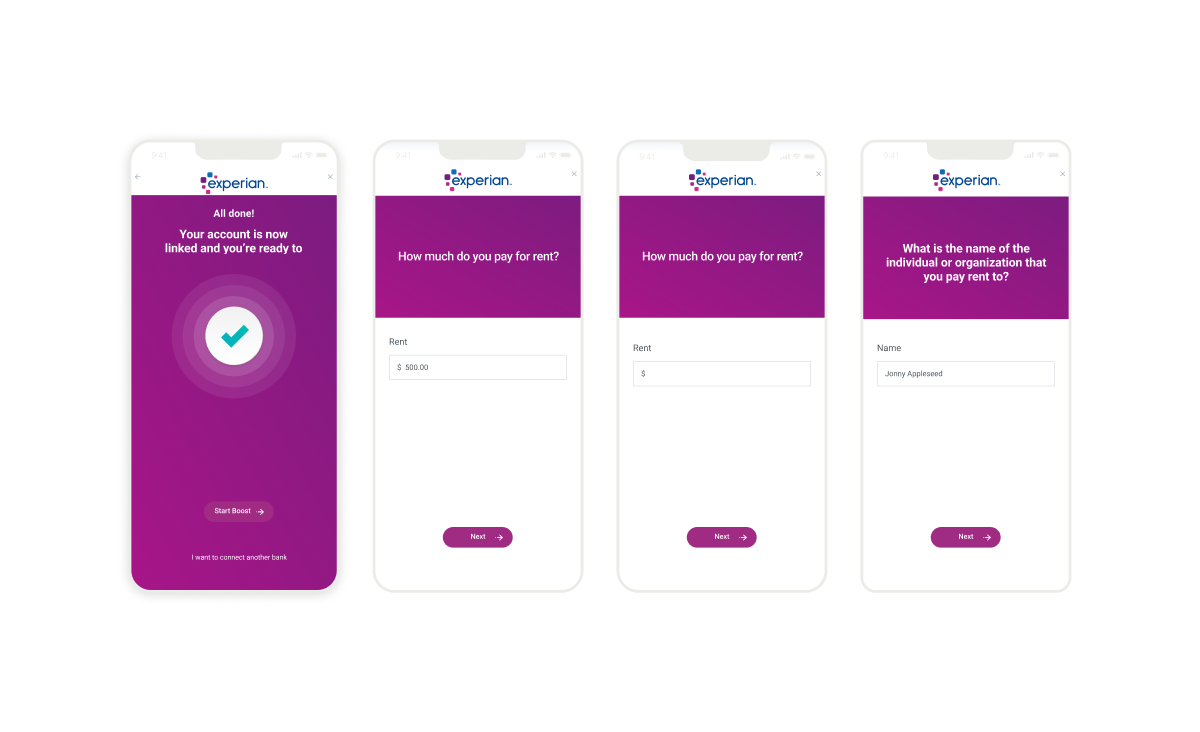

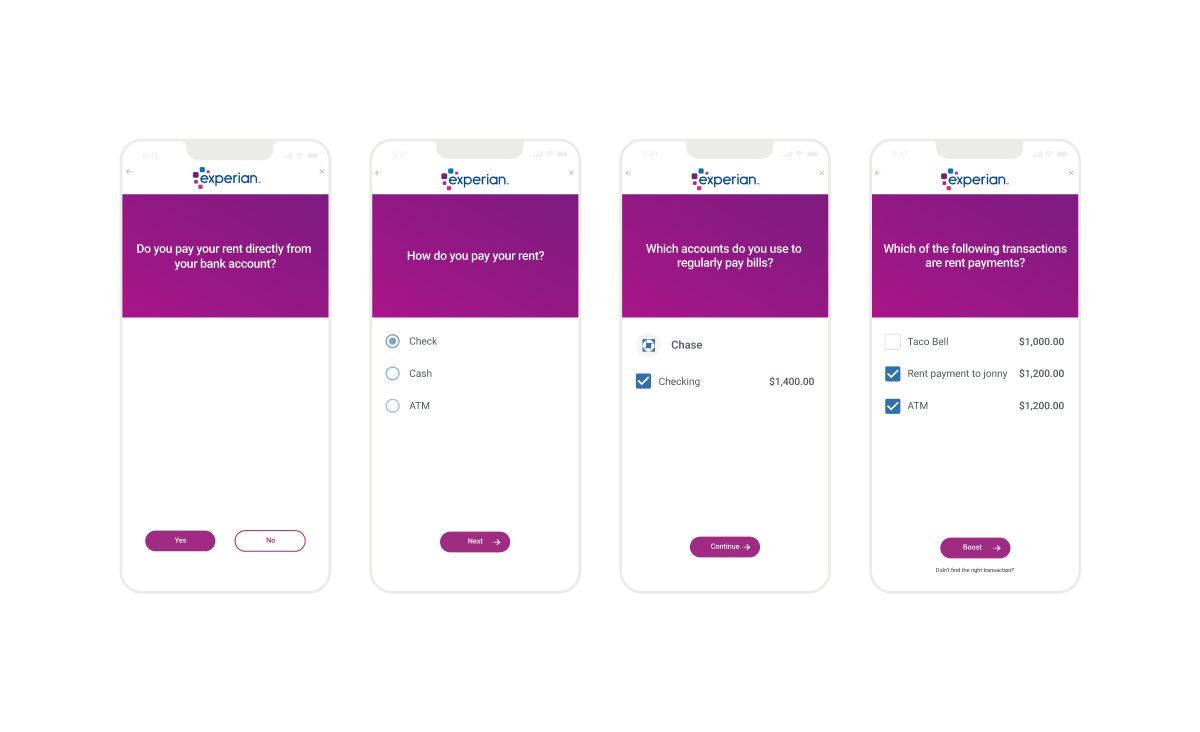

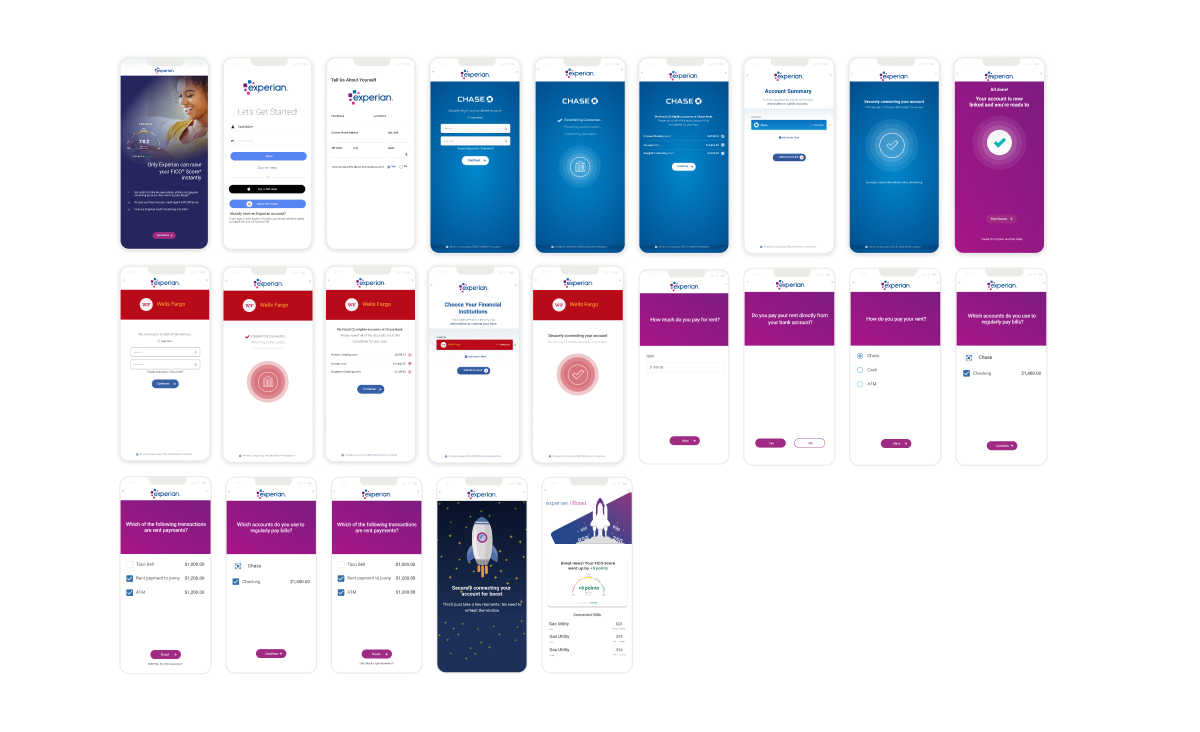

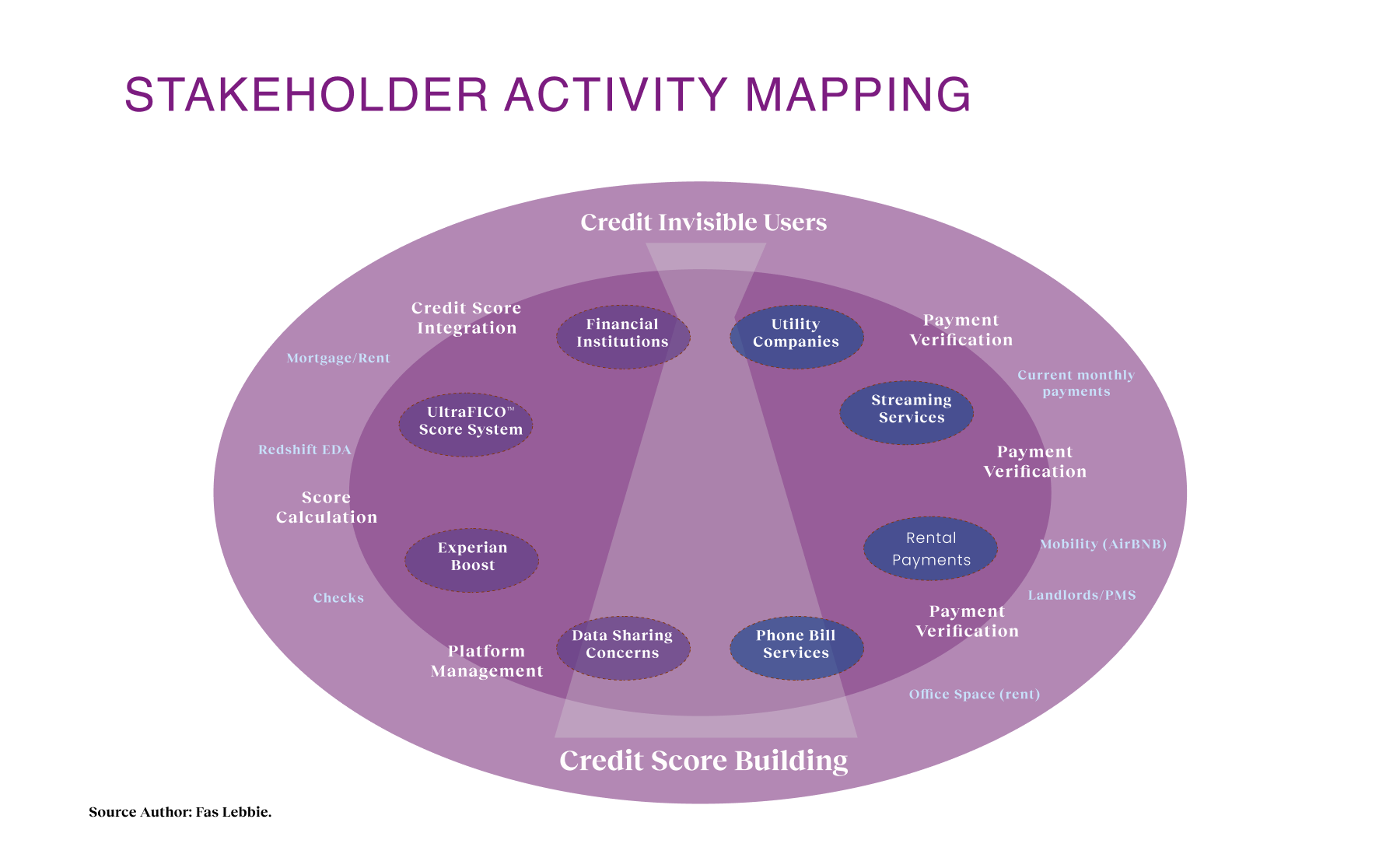

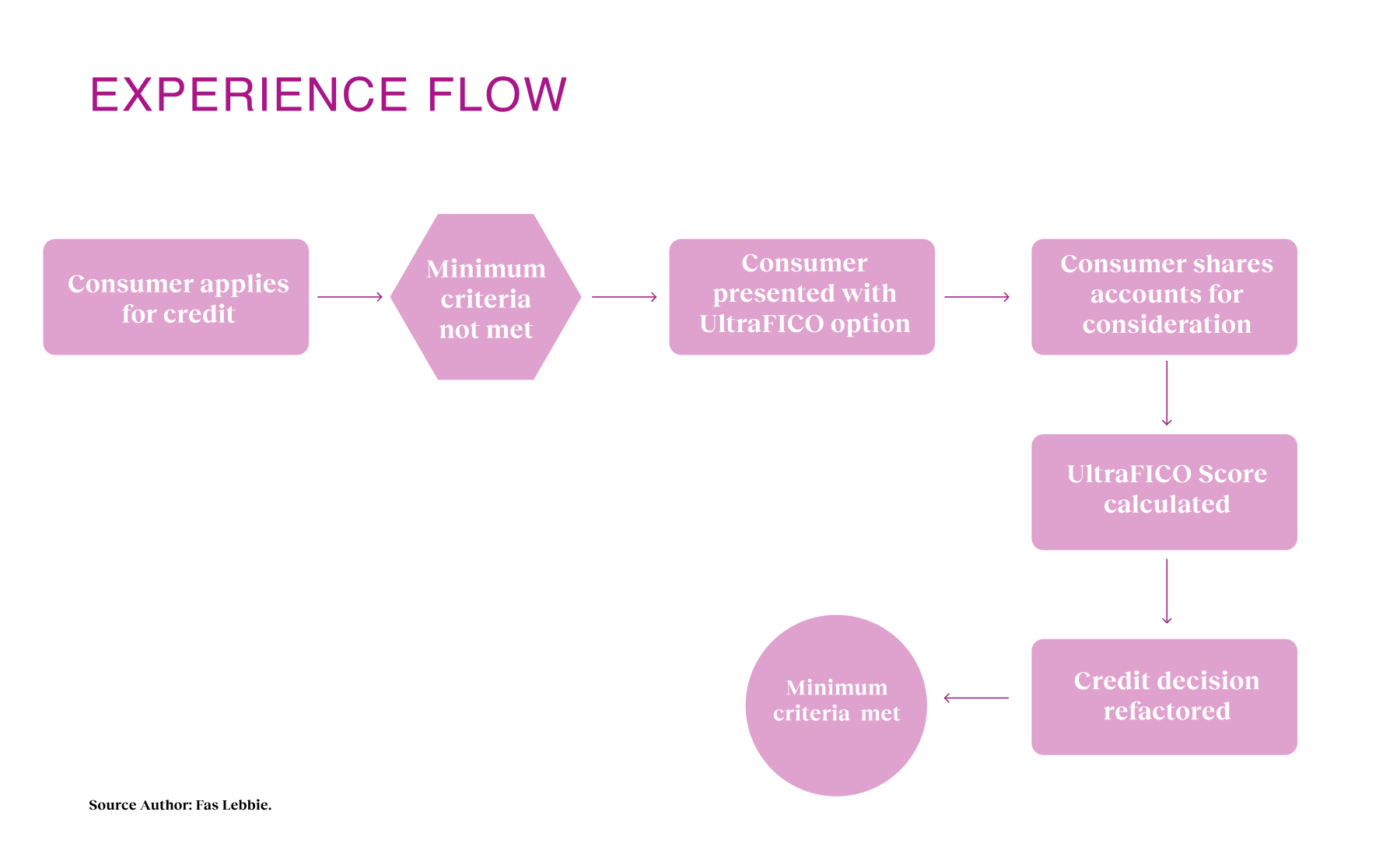

These insights presented design interventions that could be made in traditional credit scoring methods, particularly for those with a credit score of 680. We proposed an application that empowers users to link accounts and securely streamline their rent and utility transaction history. This platform would facilitate a simplified onboarding process, allowing users to enhance their credit scores through demonstrated financial responsibility. The MVP was built based on three use cases that our design solution must have.

- Experience design must incorporate best practices for usability and accessibility in the financial regulatory fintech space to ensure individuals can quickly link their financial data.

- The design must integrate utility and rent data to capture payment histories and translate regular payment behavior into credit-boosting opportunities.

- Experience design enhances security measures to ensure users’ data security and ease of use, thereby fostering trust and encouraging adoption.

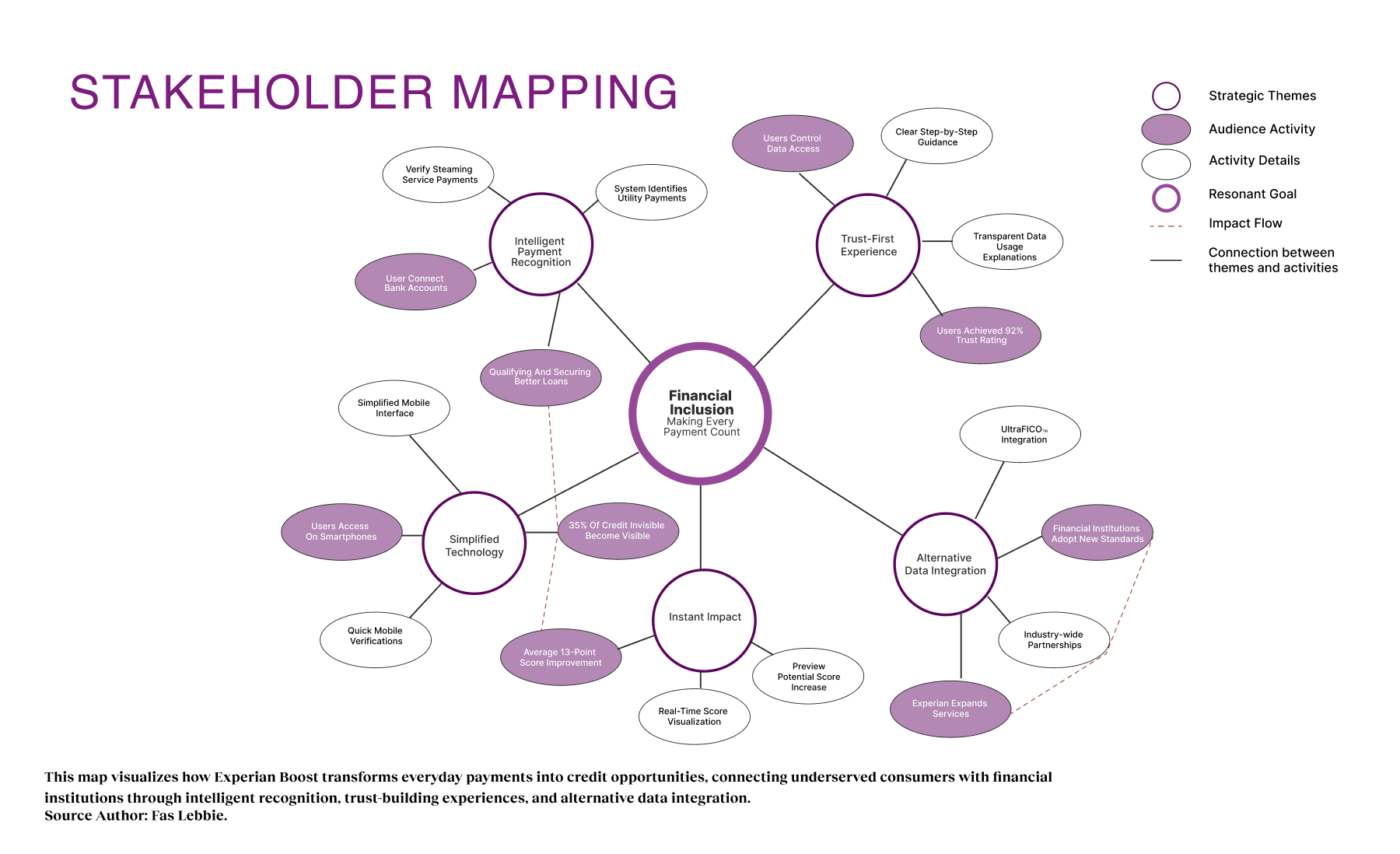

Our prototyping process emphasized three essential components: seamless and secure bank linking, clear visualization of potential credit score enhancements, and intuitive step-by-step guidance throughout the app experience. Our 28 users provided valuable feedback during testing, which led us to refine the system after each iteration. Key insights revealed that 92% of users prioritized transparency in financial services, 88% favored mobile-first solutions, and 76% required clear demonstrations of value before sharing their data. Implementation involved a phased rollout, starting with essential utility connections and gradually adding more payment types as users became comfortable. This process navigated various regulatory requirements and federal laws related to financial data exchange, ensuring compliance with the protocols of banking institutions. We established secure infrastructure to connect millions of bank accounts while safeguarding user data. Our strategy focused on building trust through progressive feature disclosure, starting with core security integrations and real-time utility data verification, while adhering to strict privacy standards. This approach resulted in high completion rates and positive user experiences, effectively bridging the gap between utility payments and credit recognition.

How it works

The UltraFICO™ Score incorporates transactional data from consumers' checking, savings, and money market accounts, extending the scorable population and refining prediction accuracy to broaden financial inclusion.

Design Interventions

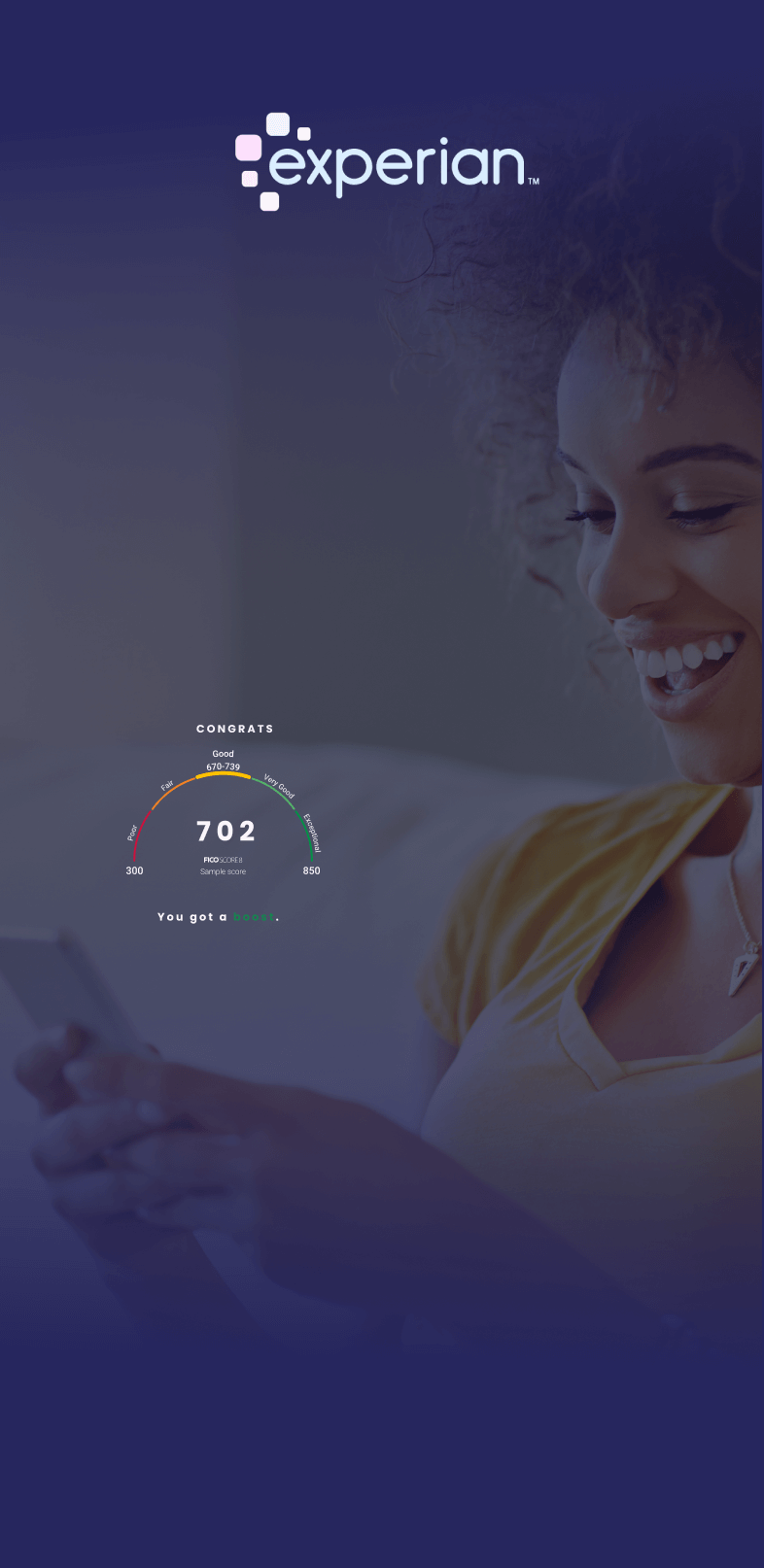

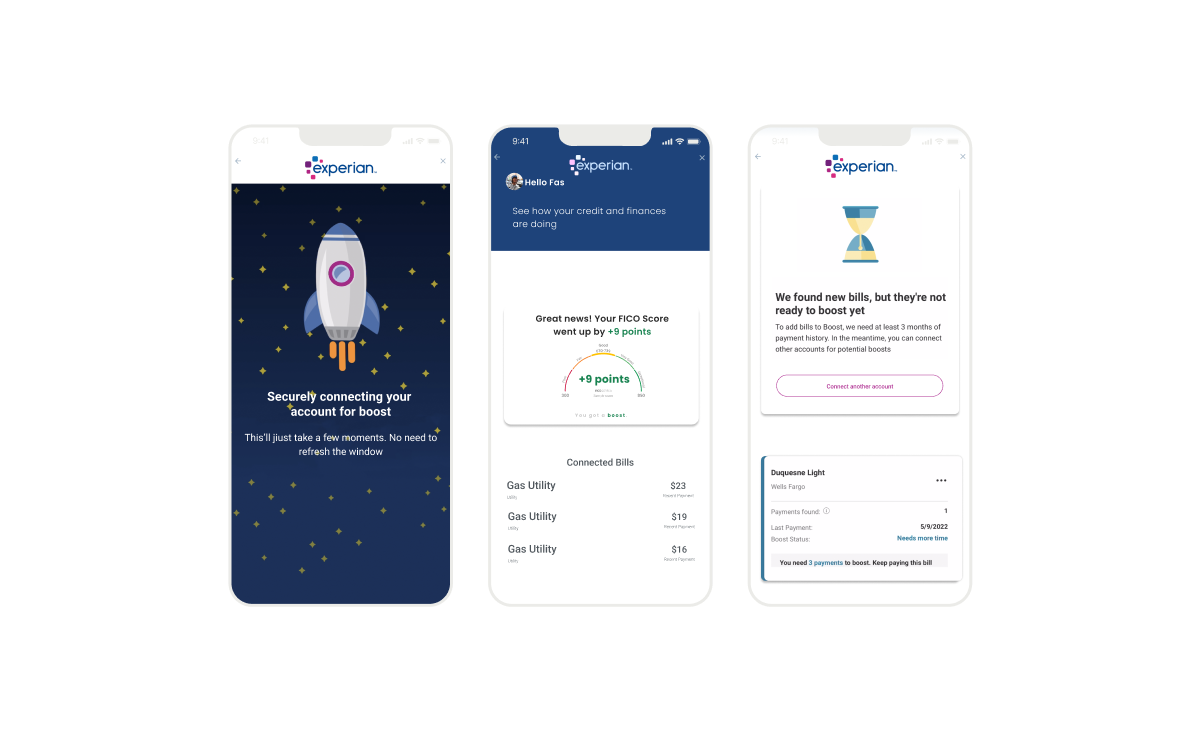

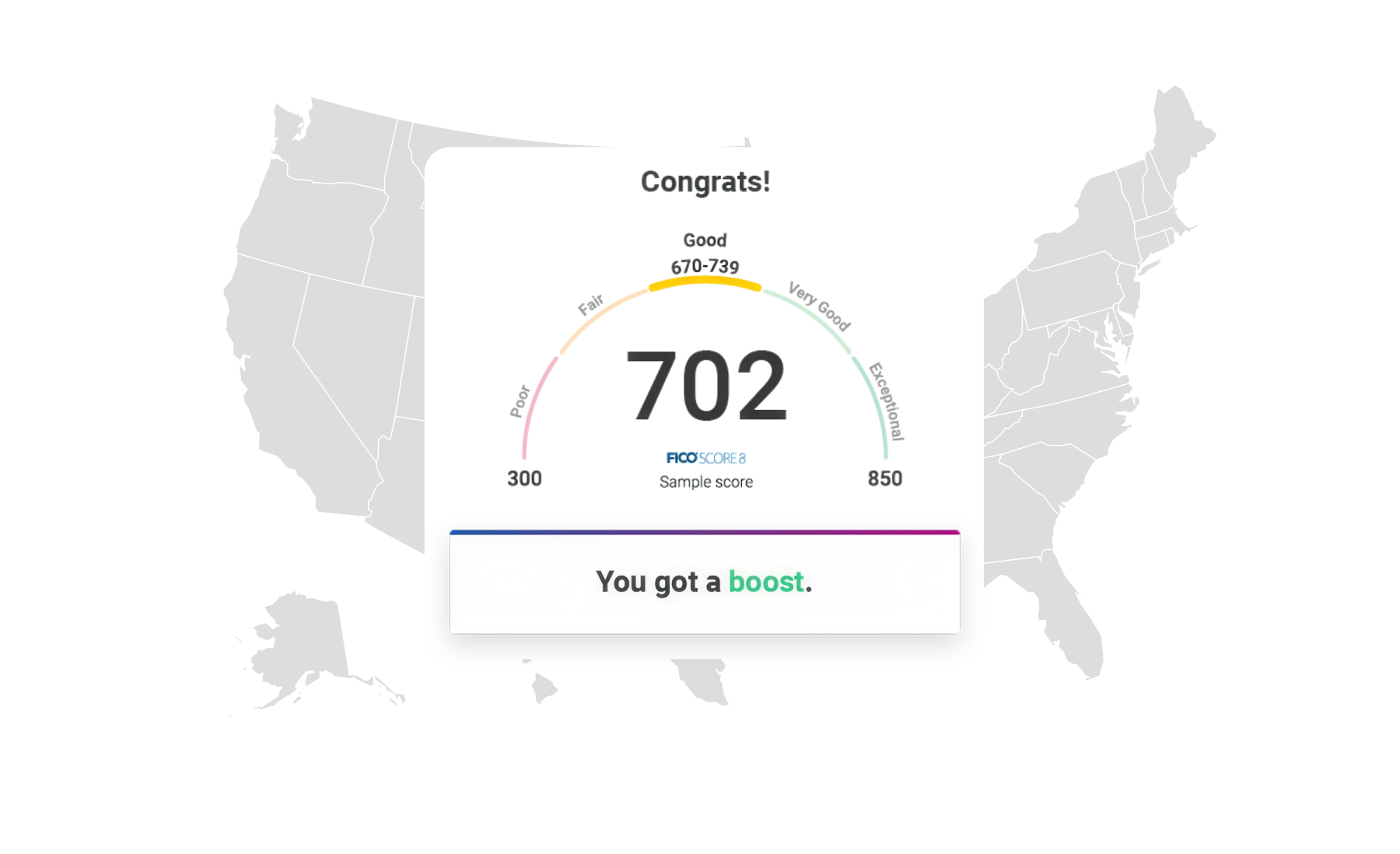

The design intervention targets renters who regularly pay rent and utilities. Currently, 35% of credit-invisible Americans do not benefit from timely payments based on their credit scores. To address this, we proposed Experian Boost. This app securely links users’ financial accounts and integrates rent and utilities payment history to evaluate financial reliability based on consistent bill payments. By recognizing these payments, credit scores increased by an average of 13 points.

Outcomes

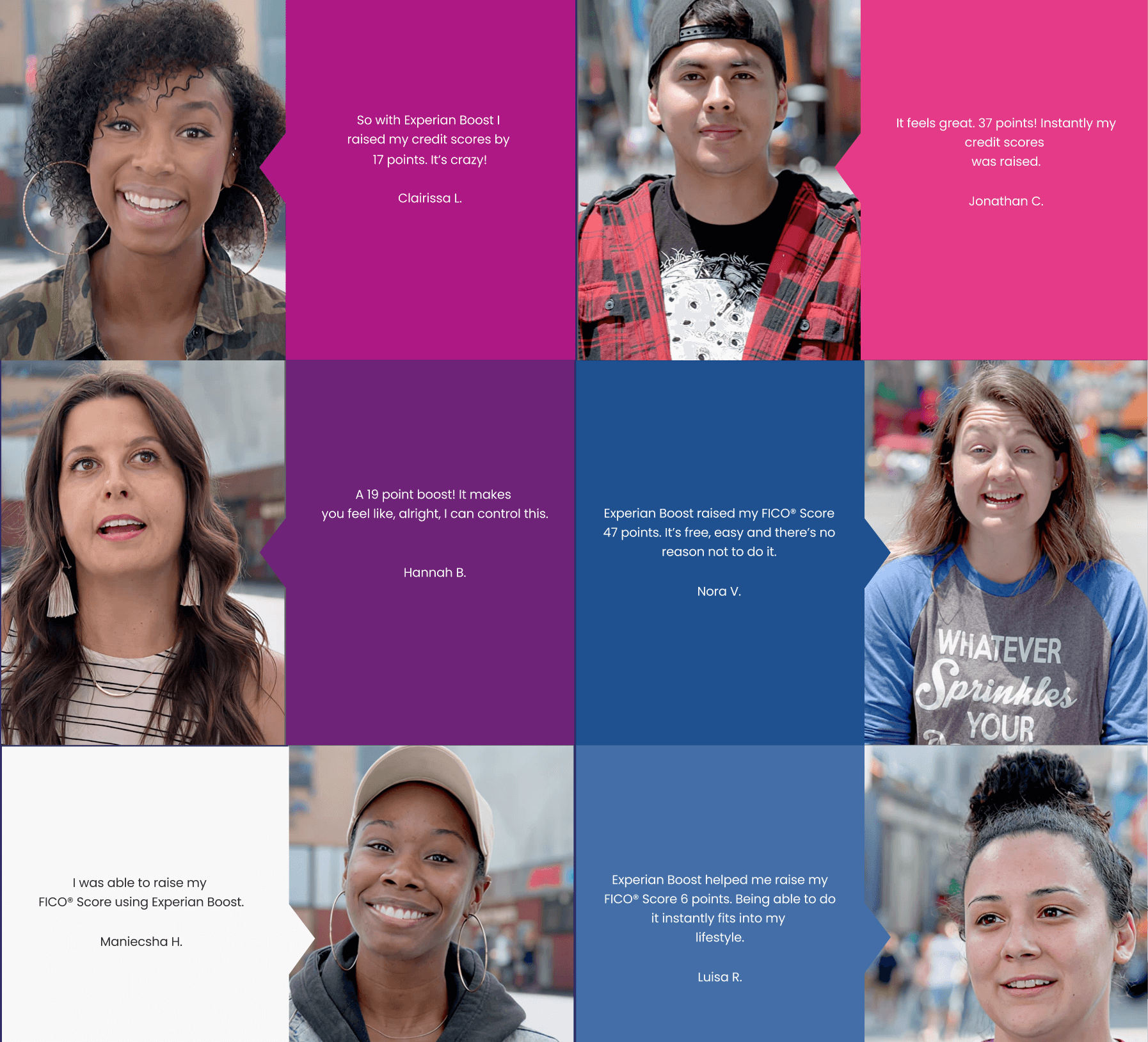

Users share stories of credit score transformations, from 6-point to 47-point improvements, representing millions of Americans gaining financial recognition and opportunity.

Toolkit, Methods, & Frameworks

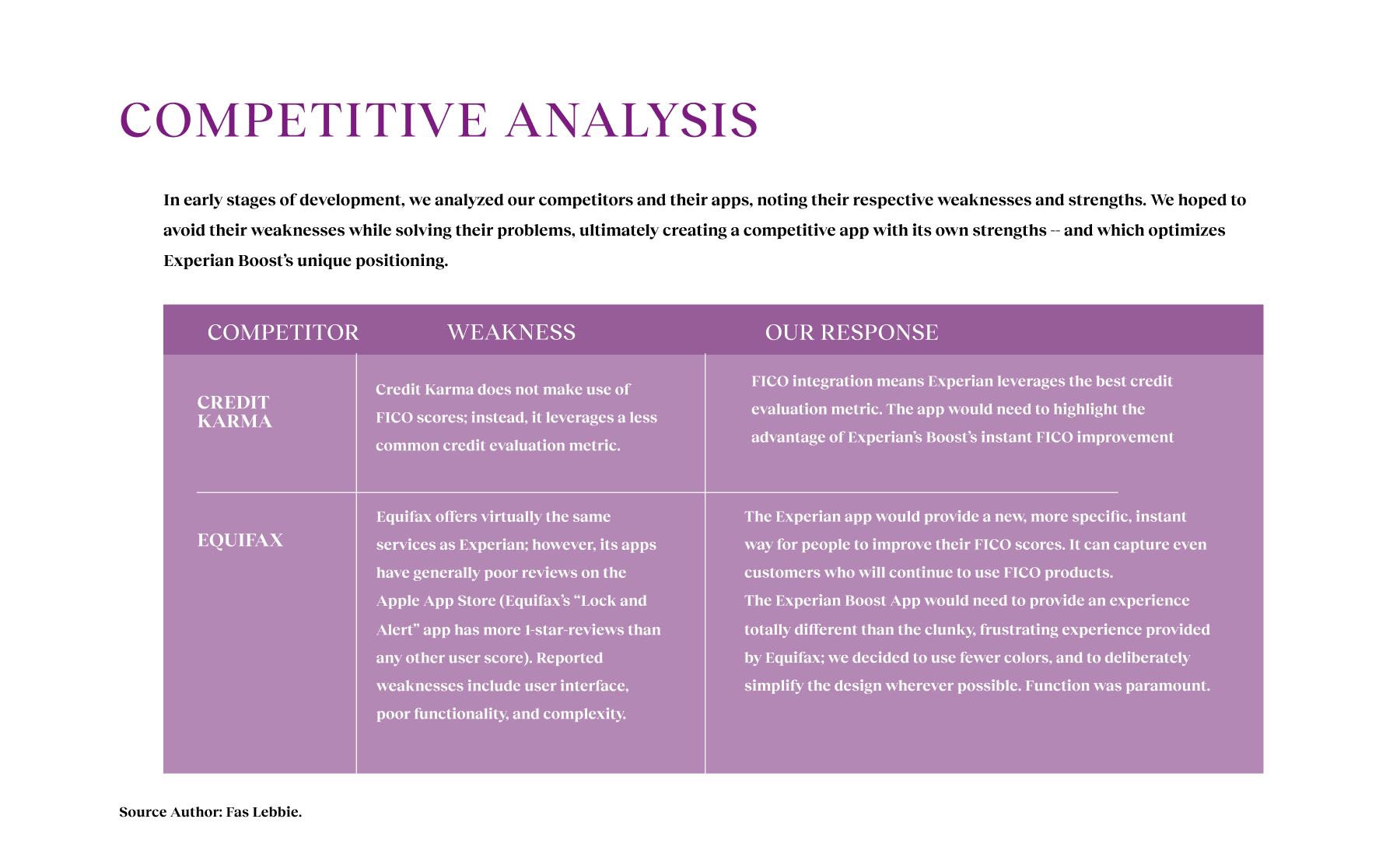

This project, at its core, leverages ethnographic research to leverage methods like stakeholder mapping, user interviews, pain scale analysis, and more, which helped uncovered barriers facing credit-invisible consumers. Competitive analysis and a theory of change framework clarified market gaps and outcomes, guiding our team’s strategy to reframe everyday payments into credit-building opportunities.

Users Impacted

Users gained financial opportunities and credit visibility nationwide.

Average Increase

Average credit score increased, which helped users qualify for apartments and loans.

Credit Score Increase

Users experiencing meaningful credit score improvement leading to growth and financial recognition.

Short & Long-term Impact

Within the first year, users saw their credit scores increase by an average of 13 points, with more compelling stories emerging of individuals qualifying for their first apartments, securing better car loans, and feeling recognized for their financial responsibility. Our 92% trust rating showed that we built something people believed in, reminding us why we design: to make complex systems work better for everyday people. Experian Boost didn’t create new financial behaviors; it just gave credit where credit was due. The project’s true impact extends beyond individual credit scores. The Partnerships with 30+ financial institutions and integration with UltraFICO™ benefits an estimated 7 million consumers in the critical 500-600 FICO® range—typically just below lender minimums—while providing a credit pathway for the 35 million Americans with no credit score at all.

Next Steps

Following our MVP launch, key opportunities included:

- Expand payment types to include more streaming services and insurance premiums to capture broader payment behaviors.

- Develop additional financial institution partnerships for direct integration of Boost into lender workflows and decision-making.

- Enhance mobile app capabilities with real-time notifications, credit monitoring, and personalized financial guidance.